I remember when I was in high school, our mother used to give us our weekly allowance and this is where I learned about budget.

From then, you have to make this money survive up until Friday. Or else you will have to stare at your classmates eating on recess while you have nothing left on you to buy a snack for yourself.

In addition, I realize that since then, our mother unconsciously teaches us how to manage money just by entrusting us our weekly allowance.

Our school is just walking distance away from our home. All we have to allot in our allowance is the daily recess.

Or when your ball pen suddenly falls and it doesn’t write anymore so you have to buy another one (sigh!).

When I got into college, the weekly allowance was also given to us. But this time, it is more challenging than in high school.

In college, I have to ride a jeep going to the town where I used to study.

It’s a one hour trip and after you reach the town, you have the option to ride in a tricycle or walk to get to the school.

There are times that my class schedule is whole day. Lunch or snacks should be included in my budget.

If there are paper works to be done or books that need to be photocopied for my reference, I have to also allocate a budget for that.

This time, my weekly allowance includes transportation, lunch or snacks, photocopy, and other miscellaneous expenses for school (yeah college life!).

I survived college life (yay!!!).

I learned to budget my weekly allowance up until I get to my review class for the board exam for CPA licensure until I landed my first job.

And I have been conditional. I have to take another exam for the two subjects that I failed to pass the CPA licensure examination. While waiting to take another exam I said to myself I need to work.

My first job was as a sales clerk. My workload needs overtime to the point where we need to stay in the office overnight for us to meet our deadlines.

For an apprentice like me, I was eager to work and the fact that more overtime, more take-home pay (the fruit of my labor :))

I remember having a monthly net pay of P 6,000.00 (including overtime). I was able to pay my rent, food, transportation allowance and sometimes I’ll be able to give some money to my mother.

How was I able to survive? I make sure that I keep all my payslip for my reference.

List down my semi-monthly net pay and subtract all the expenses, including rent, transportation, food.

I can also buy some things needed for my work, like clothes and shoes but I make sure that it is within my budget.

If there are any excess on my budget, I saved it in my other wallet for emergency purposes.

When I passed the CPA licensure exam, another opportunity came. Another job with a much higher salary. I have already bought what I want but still with certain limitations.

But as you go along, many things change and even your priority. When I got pregnant with my first born child, the very first thing that came to my mind is I have to be prepared for this.

I make sure that my priority now is to save for my incoming child and that is the time I decided to open my very first bank account (another achievement on my financial journey, yay!) and all the rest are history (kidding!!!).

I shared my story because I wanted to let our readers know the importance of budgeting. And for this article, I want to share with you the lessons I learned and on how to make a proper budget.

What is Budgeting

But before we start on the nitty gritty aspects of budgeting, let me define the word budgeting first.

Budgeting is a process of making a plan of spending money by preparing an itemized estimate of income and expenses over a period of time.

In my own interpretation, budgeting is monitoring your money coming in and controlling the money going out of your wallet until the next pay day.

Now that you know the definition of the term budgeting, let’s take a look at the pros and cons of having a budget.

What are the Pros and Cons of Having a Budget

For people who need to know the amount of money they need to go through on a monthly basis, what costs they have, and the amount of their future income will be alloted towards their monthly bills and expenses, budgeting is something you have to do.

Depending on the amount you earn, what monthly expenses you have, and how far ahead you like to plan, setting up a budget is a simple method to know what you have and where your money is going.

Here are the Pros of Having a Budget

There are a few pros that you will discover when you start budgeting. Some of these are:

- You see precisely where your cash goes. These are lease, goods, emergency funds, and so on;

- You will realize precisely the amount you need to go through every month. And the amount you can save;

- You can plan with paying bills, and allocate the payment to specific debit or credit cards every month; and,

- You don’t need to stress over whether you have adequate money for the payments you have.

By having a budget, you will realize you have a specific measure of salary every month for every classification, and once that sum lapses, you are out of assets.

Here are the Cons of Having a Budget

There are a couple of downsides you have to consider with budgeting including:

- Unexpected bills (as life is brimming with crises and sudden events, you can’t be sure whether something will turn out badly);

- You may overcompensate in certain categories, and not have adequate money for different expenses you have to make;

- You may run in to a surprising budgetary need, (for example, doctors fees or car inconveniences), which you can’t prepare for; and,

- You need to put time aside to make these budgets, and stick to them, in the event that you need your own budget to be useful and to work.

The art of budgeting is one that you should learn.

Despite the fact that there are sure disadvantages, you can generally build an emergency fund, or you can utilize other budgeting techniques also (envelope strategy, a crisis credit card, and so on).

Yet, if you budget, you are going to see where you are going through every month, where you are spending excessively and where you need to cut back.

And you will also learn what you are doing wrong every month.

Learning how to make a budget and continuously learning about it is something you will do each month.

After some time, you will become familiar with your mistakes, you will perceive what changes must be made, and you will even discover certain techniques which will allow you to start a bank account (or saving cash for investment funds).

Since you have appropriately figured out how to make a proper budget. Despite the fact that it requires some investment in time to learn, people who do it discover that it is worth it regardless of the time.

And it is the best way to monitor and manage your money.

What is the Importance of Budgeting

Control of your money

Because budgeting is the same as spending plan for your money, it helps you to be aware where your money is being used.

As a result, you will be able to control your cash flow.

Distinguishing needs versus wants

Budgeting allows you to differentiate needs and wants. When you are in control of your cash flow, you will be able to prioritize your needs.

Basic needs are very important for you to survive. These are your budget for food, transportation, rent, and so on.

These are the things that you literally die for. As for the wants, you can always allot a budget for it too.

Plan for your vacation, evaluate how much you need and then save up for it by making room in your budget.

That is the beauty of budgeting because it allows you to spare some room for your wants.

Keep out of debt

Budgeting keeps you out of debt.

This can be done by applying the other points mentioned above which are control of your money and distinguishing your needs versus wants.

If you do not follow a spending plan, it is easy to get yourself out of track and before you even realize it, you are already in debt.

Following a budget is a great way to keep out of debt. It also allows you to create a plan to pay off debts.

How To Make A Proper Budget

Having a proper budget helps you manage your money carefully. And the first step in taking control of your financial life.

It can help you zero out your outstanding debt, put money into savings, cut down your expenses, and make your money work for you.

Budgeting may not be the more entertaining thing to do. It takes a lot of patience, discipline, and self-control for you to master it.

But once you get used to it and make it a habit, it will all be worth it.

I have laid out a step by step guide to help you make a proper budget. Try to follow along. Let’s start:

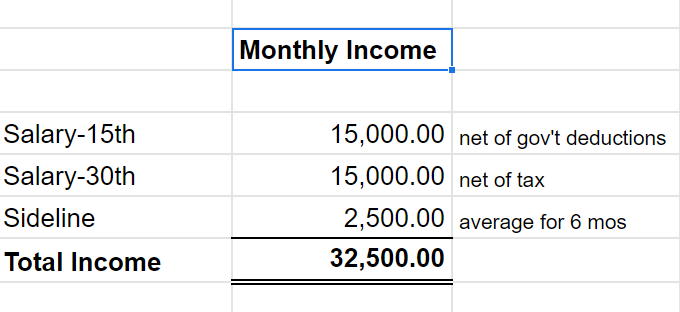

1. Determine your monthly income

If your income comes from a monthly salary, you have an idea of the fixed amount you are receiving. This amount is net of all the deductions: government contributions, loans, and withholding tax.

If your income is coming from the profit of your business or if you are a freelancer, you can compute your income on average. You can base it on the three to six months income you received and get the average amount. This will be the basis of your monthly income.

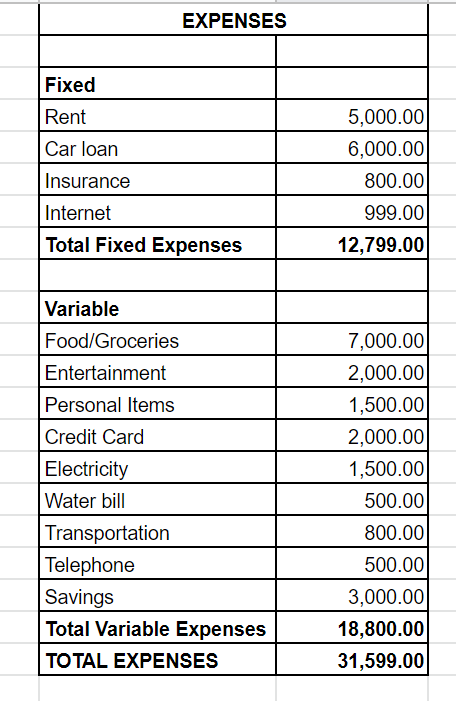

2. List down all your expenses

You may categorize your expenses into fixed and variable. Fixed expenses are those items that occur regularly in a month like rent, mortgage, insurance, and the internet bill. Variable expenses are those monetary amounts that change from month to month. These are usually the areas that you can cut back or adjust to save money.

3. Set your goals

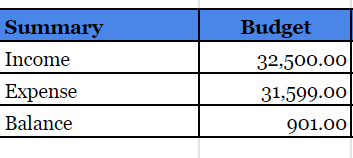

Once you have the list, subtract your income from your expenses. If this is positive, you are on the right track. But if it is negative, you have to review your list of expenses and try to reconsider cutting back some of it.

Now you have to set your goals. It may be a short-term goal like being debt-free, buying certain appliances that you need in your house.

Or a long term goal like saving for your retirement, college fund for your children, or you want to build your dream house.

Once you list down your goals, make a target amount, and the target date for its completion. Your goals should be SMART.

- Specific

- Measurable (amount)

- Achievable

- Realistic

- Time-bound (date)

These goals will play a part in your budgeting system since you need to allot a certain amount of money for these things to achieve.

4. Actual vs. Budget

Now that you have your list of budget income and expenses it is time for you to track the actual cash in and cash out. And now you have goals that need to also prioritize, sticking with your budget is a must.

And now that you have a comparison of your expenses based on your budget, from time to time try adjusting your budget until it fits your monthly financial plan.

Remember that this monthly budgeting is not a one-time big-time task. You should make it a habit until it becomes your routine.

And that is how to make a proper budget.

Here is a FREE stuff for you!

To help you more, I prepared a budget template on a spreadsheet that you can download and use. It is completely editable. And the best part is it’s FREE!

I hope that it may help you in starting your journey of budgeting. You can edit or customize the list depending on the category of your income and expenses.

Now that you have created your first budget, start implementing it right away so you will get used to it in a couple of months.

Try to make a budget for the next 6 months considering all the expenses you might incur.

Annual expenses like car registration, hospital check ups, real property tax, and other fees that are not on your regular routine.

From this point on, you will get a good feel about your financial status. You will be able to verify if you are on the right track in managing your finances.

As you go along, try to improve your budgeting skills by cutting off some bills and allotting it to important things in life such as treating your family by going on a vacation.

How to Determine High Priority Bills Versus Low Priority Bills

Determining the prioritization of paying bills is easy.

Here is a step by step guide to help you outline it and help you make an effective and proper budget.

Step 1

First is to list down your bills. You already have this list if you followed along the steps on how to make a proper budget.

But in this section I will help you break it down a bit more.

List down your bills according to the following categories:

- Basic needs – Such as groceries, rent and transportation.

- Utility bills – Such as electricity, water, phone and internet.

- Debts – Such as mortgage, loans and credit card debts.

Step 2

Next is to identify your Must Pay bills. Basic needs and utility bills should always be considered. There are no negotiations here.

What I need you to concentrate on are your debts. And now, let’s move on to the next step.

Step 3

Next is to break it down a bit more according to the amount of penalties or interests if you failed to pay on time.

Make the list from highest amount of penalties to the lowest.

From there, you will have figured out the high priority bills versus low priority bills.

The most logical strategy is to pay the highest amount of penalties first.

What are the Types of Budgeting

Did you know that there are 2 types of budget? They are called the basic budget and current budget.

We will start by defining the 2 types so we will know the difference and when to use each one.

Basic Budget

Basic budget is a budget you set on a yearly basis.

This is considering all the expenses including the monthly budget, quarterly budget, semi annual budget and annual budget.

Basic budget is prepared to forecast expenditures for a number of years. This is usually used by companies and government offices.

But it can also be for personal use.

This is perfect when you want to save up for the college fund of your kids or for your retirement.

Current Budget

Current budget is a budget available to spend for the current month. It can also be called adjusted budget.

This is because there are unexpected expenses sometimes. Like in today’s situation, the whole world is suffering from the pandemic caused by the corona virus 2019.

For personal finance, unexpected expenses also arise from time to time. For example is when your laptop or your mobile phone breaks down which you are using for work or for your business or for your side hustle.

In this case, you need to adjust your budget according to your needs.

Can you adjust your budget?

You need to take a good look at your budget routinely and adjust your budget if things change. Change may be good or bad.

It is a good thing if for example you had a promotion that increased your income. It is a bad thing if the change is negative.

For example is when you experienced a job loss.

You likewise need to consider your future plans and ensure that you sufficiently save money to have the option to meet your financial goals.

Remind yourself that you set your own financial goals, so it is dependent upon you to meet them.

It may mean abandoning a portion of the things you need, which will be troublesome for the time being, yet you will be happy in the long haul on the off chance that you meet your financial goals.

You can adjust your budget by carefully taking control of your money.

Then work out a plan to handle such life events and changes so you can adjust your budget accordingly.

Budgeting Rule For Personal Use

I would like to introduce to you a budgeting rule that you can do for personal use. It is called the 50 / 30 / 20 Rule.

This rule is popularized by Elizabeth Warren in her book entitled All Your Worth: The Ultimate Lifetime Money Plan.

The 50 / 30 / 20 budget rule is a simple plan to help people achieve their financial goal without the hassle of too much mathematics while having a happy life.

The budget rule is to take a percentage of your income and allocate it to spend for 50% on needs, 30% on wants, and 20% on savings.

Needs are the basic necessities in order for you to survive like food, rent, transportation and utility bills.

Wants are the one that will make you enjoy life so you will not be burned out. When you are burned out or if you are really tired and feeling deprived, you tend to quit.

People tend to quit when things get rough.

These are things like treating yourself to eating good food, watching a movie in the cinema with your family, going on a short vacation or buying that new shoes you have been meaning to buy.

Savings are for building your emergency fund, life insurance or for investments.

This can also be used for when you are saving up for large purchases like buying a house or buying a new car. To make it short, this is for your financial goals.

4 Simple Steps in Making a Budget

In making a budget, there are many things to consider. But there are only 4 simple steps in making a budget.

Step 1 – Money In

Consider your income. How much money is going in your pocket? List all your income whether from a salary, profit in your business, payment for a side hustle or a dividend or interest payment from your investments.

Step 2 – Money Out

Consider your expenses and list it down. How much money is going out of your pocket? These are the bills you have to pay. Groceries, gas, rent for your apartment are the things to consider.

Do not forget about your annual expenses like car registrations, insurance and real property tax. Savings is another thing to think of.

Step 3 – Assess

Is your money out less than your money in or at least they are equal? Then congratulations! You are on the right track!

But if your money out is more than your money in, then you are in a deep hole. This part is quite tricky and it will depend how deep you are in. And that will determine your following actions. The deeper the hole, the more drastic action needs to be done.

Step 4 – Using and Maintaining

Once you are done listing your money in and money out and you are done with your assessment, it is now time to use and maintain it. Stick to it like glue and soon you will find yourself free from financial troubles.

Should you Lend Money to Someone While Staying in a Budget

This is a tricky topic especially when you are on a budget.

My quick advice is to avoid lending money to your friends and family. Unless you are on a loan business of course.

But if this is not the nature of your business or trade, I would certainly advise not to lend money. Especially when you are just starting out on learning how to make a proper budget.

Considering the title of this article, my educated guess is that you are not yet in a place where you can manage your finances very well.

However, if you are already in a stage that is beyond this, then I can say that it is okay to lend money to your friends and family.

10 Practical Tips to Stay in Budget

In this section of the article, I will share some practical tips to stay in budget. The following are general things you can do to track yourself and stay motivated.

- Remember why you are doing this

- Pay yourself first

- Set a daily and weekly budget

- Keep your receipts and record all your expenses

- Plans meals ahead of time

- Involve the whole family

- Read personal finance blogs

- Watch money saving hacks videos

- Use budgeting apps in your favor

- Do not forget to enjoy the chase

Top 7 Budgeting Apps of 2020

Mint – Budget, Bills, & Finance Tracker

Best Overall

Mint is the free money manager and financial tracker app from the makers of TurboTax® that does it all. We bring together your bank accounts, credit cards, bills and investments so you know where you stand. See what you’re spending, where you can save money, and track your bills in Mint like never before.

PocketGuard – Personal Finance, Money & Budget

Best to Keep From Overspending

PocketGuard is a free app that makes it easy to take control of your personal finance and stop overspending. Its intuitive money management tools help you make a budget, track spending and build savings automatically.

YNAB (You Need a Budget) – Budget, Personal Finance

Best for Type-A Personalities

YNAB will help you break the paycheck to paycheck cycle, get out of debt, and save more money.

Wallet – Money, Budget, Finance & Expense Tracker

Best for Just Budgeting

Wallet is a market-leading personal finance manager, built to help you save money, plan for the future, and see all your finances in one place. With Wallet you can track your daily spending automatically with bank synchronization, dive into weekly reports on your spending, manage debt, plan your shopping and share specific features with loved ones.

Best for Cash Style Budgeting

Mvelopes uses an envelope budgeting method to help you plan and track your household or personal budget. You can assign and manage your budget, as well as receive feedback on where you have spent your money and how much you have remaining.

Best for Couples

Goodbudget (formerly EEBA, the Easy Envelope Budget Aid) is a money manager and expense tracker that’s great for home budget planning. This personal finance manager is a virtual update on your grandma’s envelope system–a proactive budget planner that helps you stay on top of your bills and finances. Built for easy, real-time tracking.

Personal Capital – Investing and Finance App

Best for Investors

The Personal Capital Investing app – this is the smart way to track and manage your personal finance. Now you can see all your accounts in one place—bank accounts, stocks, retirement funds, and your investments.

Top 3 Most Famous Books About Budgeting

All Your Worth: The Ultimate Lifetime Money Plan

Author: Elizabeth Warren

Description: This personal finance guide offers a new way of thinking about and managing your money that will allow you lifelong emotional peace and financial well-being.

The Everything Budgeting Book: Practical Advice For Saving And Managing Your Money

Author: Tere Stouffer

Description: This is a fundamental guide for individuals who need to quit living paycheck to paycheck and begin enjoying the cash you didn’t know you had. With this bit by bit guide, you will have the option to improve your spending patterns, get ready for crises, and plan for what’s to come.

How To Manage Your Money When You Don’t Have Any

Author: Erik Wecks

Description: Specifically for those who struggle with paying their bills, this book provides a reality-based path to financial stability in today’s turbulent economy. Plus, unlike some of the other finance fanatics on the list, Wecks is not wealthy and is not here to teach readers how to build wealth. He is providing guidelines to do the best one can with the income one has.

Budgeting Basics Explainer Video

The following video is from Two Cents Youtube Channel

Budgeting Basics

Best YouTube Channels to Save You Money

Mint.com

https://www.youtube.com/channel/UC8-KKHWmrCCeot0_H5rHcyg

The Financial Diet

https://www.youtube.com/channel/UCSPYNpQ2fHv9HJ-q6MIMaPw

Household Hacker

https://www.youtube.com/user/HouseholdHacker

The Dave Ramsey Show

https://www.youtube.com/user/DaveRamseyShow

Two Cents

https://www.youtube.com/channel/UCL8w_A8p8P1HWI3k6PR5Z6w

Chink Positive

https://www.youtube.com/user/visionchinkee

Tipid Tips atbp.

https://www.youtube.com/channel/UC5M9VfaYftZY74t_rHoqCSA

Should you stop budgeting when you win a lottery?

Everybody wishes to win a lottery, admit it. Who doesn’t want to, by the way?

And if you are one of those very lucky people to win the lottery, should you stop budgeting?

Before I answer the topic, I would like to share with you some things to do when you win a lottery.

1. Save for retirement

The first you should do is to save up for your retirement together with your partner in life.

This will ensure your financial well being in your old age. Secure that health care insurance.

2. Set aside for your family

If you still have parents, provide for them like buying them health care insurance. Give them something that will be benefited in the long run. As for your kids, take a portion of your winnings and set aside an investment for them.

3. Acquire good assets

In more popular terms, you should invest. Buy stocks, build a business, buy a property that will generate you passive income. In this case, you will not need to be employed again.

4. Build a team

If in case your lottery winnings are really great like in millions, you should opt to build a team for you. Hire an accountant, a lawyer, and a financial planner. Even if you are really good at money management, building a team to manage your newly acquired wealth is a good idea.

5. Pay off debts

This is the best time to pay off debts or loans or mortgages you may have. This move will significantly make you feel better both emotionally and financially.

6. Share you blessing

Give a portion of your winnings to charitable institutions. Offer tithes to your church. Share your blessing to other people especially to those who are in need.

And now, to answer the question, it is recommended to not stop budgeting even if you won the lottery. The money you won in the lottery might be spent on things that don’t really have an impact on your life. You may celebrate and enjoy your winning but be sure to not stop budgeting when you win the lottery.

How to stay motivated and stick to your budget

Making a proper budget is the easy part. The hard part is to stick to your budget. This is where many people slip because sticking to a budget for a long period of time is really hard.

For this section of the blog post, I am going to share some tips and tricks to stay motivated and stick to your budget.

1. Don’t spend more money than you have.

2. Make a grocery list and stick with it

3. Bring just enough money when you go in a grocery

4. Leave your credit cards at home

5. Don’t go in a mall

6. Develop a taste for regular coffee

7. Avoid Starbucks

.8 Don’t buy things on impulsive

9. Use cash when buying something

10. Watch money saving tips videos

11. Read personal finance blogs

12. Join a group with same goals on Facebook

13. Remember your reason why you are doing this

14. Be happy from the bottom of your heart

15. Don’t pity on yourself

16. Talk to your loved ones about your goals

What to expect in the first 3 (or 6) months of budgeting

Struggles. Yes, I think that is direct enough. The struggles you will be facing may be 2 or 3 things from the following list.

1. You will overspend

2. You will budget more money than you have

3. You will forget some items

4. You will be nervous for next month

5. Your goals might change

6. You might received a surprise bill

7. You will want to quit

But there is good news. There is a way to overcome these struggles. And that is to not do this alone.

I appreciate that you are here reading this article up until this point.

I can say that you are very much willing to change your life by learning how to make a proper budget.

Join a financial education class or simply join a group on Facebook that have the same goals as you.

The simple psychology on this is you will be more motivated knowing that someone out there is also experiencing the same problem as you do.

It helps to find someone that shares the same experience. From here, learning will be continuous.

You will definitely be overloaded with information and eventually will be tired of all the gurus and experts teachings.

And when this happens, you can just step back for some time and then continue learning again. It’s okay to take a rest, Just don’t give up.

Final thoughts

I would like to end this article by the following quote from Jim Rohn for you to become motivated.

Your life does not get better by Chance, it gets better by Change.

Jim Rohn

And if you like the article, please leave a comment.

And if you really like this post, I would appreciate it a lot if you could share this article on your favorite social media network.

I hope you learned something. For any questions or suggestions, please comment below and subscribe to our page for more “My Tipid Tips”. And you may also connect with us in My Tipid Tips Facebook Page.

This article is composed in collaboration of Denver and Judith.

Happy savings!!!

Pingback: How To Do A New Normal Beauty Makeover On a Budget | My Tipid Tips

Pingback: How Does Tracking Your Expenses And Income Can Help You | My Tipid Tips

Pingback: Creative Grocery Shopping Tips To Save Money | My Tipid Tips

Pingback: Budgeting Basics To Help You Manage Your Money | My Tipid Tips

Pingback: A Good Lesson In Money Management | My Tipid Tips

Pingback: How To Start Saving In This Time of Pandemic | My Tipid Tips

Pingback: 5 Ways To Save Money On Your Car’s Gasoline | My Tipid Tips

Pingback: 10 Ways to Save Money If You Are On Quarantine | My Tipid Tips

Pingback: 5 Ways To Save Money On Your Motorcycle Gasoline | My Tipid Tips

Pingback: How to Build an Emergency Fund | My Tipid Tips

Pingback: 4 Remarkable Money Saving Tips For Every Homeowner | My Tipid Tips

Pingback: What is Financial Literacy and its Importance | My Tipid Tips

Pingback: Saving Money Should Be Part Of Your Family Budget | My Tipid Tips

Pingback: Life Is About Mastering Money And Use It Properly | My Tipid Tips

Pingback: Ways To Make Money Now Rather Than Later | My Tipid Tips

Hii

It is very good article.

Thanks for writing this article.